AI compute demand is starving mature-node DRAM capacity, creating a structural supply gap in consumer memory. To secure stable allocations, downstream OEMs are pivoting to older DDR2/DDR3 inventories – driving sharp price surges across legacy chips.

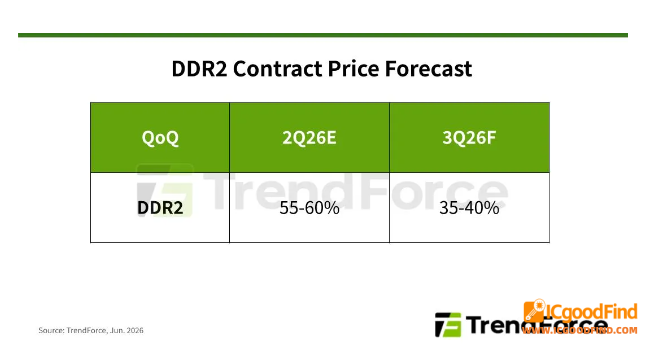

Q2 contract prices for DDR2 jumped 55–60% after Q1 gains, with another 35–40% hike expected in Q3. The root cause: Samsung, SK Hynix, and Micron continue shifting advanced wafer capacity to high-margin HBM and server DRAM, while cutting DDR4 mature-node output. Consumer electronics buyers are now rushing to Taiwanese suppliers like Winbond and Nanya – but total available supply falls far short of demand.

Both Winbond and Nanya have leveraged tighter supply to boost bargaining power, actively trimming low-margin legacy output to prioritize higher-value products. Under dual pressure from shortages and rising costs, OEM/ODMs are downgrading memory specs – moving multiple device designs from DDR4 to DDR3, and even embedding DDR2 in some products. Shortage pressure cascades down every generation.

Supply dynamics diverge:

Winbond – gradually reducing DDR2 production to reallocate to DDR3/DDR4/LPDDR4

Nanya – holding firm with selective allocations

Elite Semiconductor – maximizing foundry quotas to fill the DDR2 gap left by Winbond

Broader memory market Q2:

PC demand remains weak, but major producers deliberately cap shipments to PC brands and module houses, forcing buyers to pay up. North American cloud providers are accelerating AI inference deployments – boosting high-capacity RDIMM orders – while foundries lock long-term agreements with top clients, keeping server DRAM tight.

Smartphone brands face rising memory costs and are adjusting production cadence from Q2, yet mobile DRAM contracts continue climbing as suppliers narrow inter-segment price gaps. GDDR capacity stays limited, and higher memory costs are already pressuring notebook and gaming hardware demand.

Consumer-grade memory – traditionally low-margin high-volume – now sees cost inversion for some end-users, slightly cooling procurement. But the majors' structural shift away from consumer DRAM remains unchanged, and the supply-demand imbalance shows no near-term relief.

ICgoodFind Takeaway:

The AI tailwind is repricing every memory tier – from HBM down to DDR2. Legacy parts are no longer "cheap." Procurement teams must recalibrate BOM strategies, because this cascade won't reverse until capacity expands – and that's years away.